Quiltt for B2C Underwriting

Cash-flow underwriting works better with more data.

One provider can't reach every account, and raw transactions on their own aren't a credit decision. Quiltt routes across financial aggregators and enriches the results into cash-flow signals, opening your underwriting models to more applicants. More data. More meaning. More borrowers you can say yes to One API. Multi-aggregator coverage, plus the enrichment layer that turns 24 months of raw transactions into the cash-flow attributes your model underwrites on.

01

Reach every account a borrower banks at.

Your borrower's paycheck lands at a neobank. Their savings sit at a regional credit union. Their checking account is at a bank your aggregator has never heard of.

A single-provider integration misses at least one of those. Quiltt routes the connection across Finicity, MX, Akoya, and Plaid, picks whichever has the strongest link to that institution, and returns a normalized transaction record your model can act on. "Your bank is not supported" stops being an error your borrower ever sees.

What you get:

24 months of transaction history, normalized across providers into a single schema

Smart routing to the aggregator with the strongest connection for each institution

Automatic fallback when a provider degrades, with no dead ends and no manual

Bank customers, credit union members, and neobank users, all reachable from one integration

Build cash-flow attributes for thin-file and inclusive credit decisions with a reliable, multi-aggregator data flow.

02

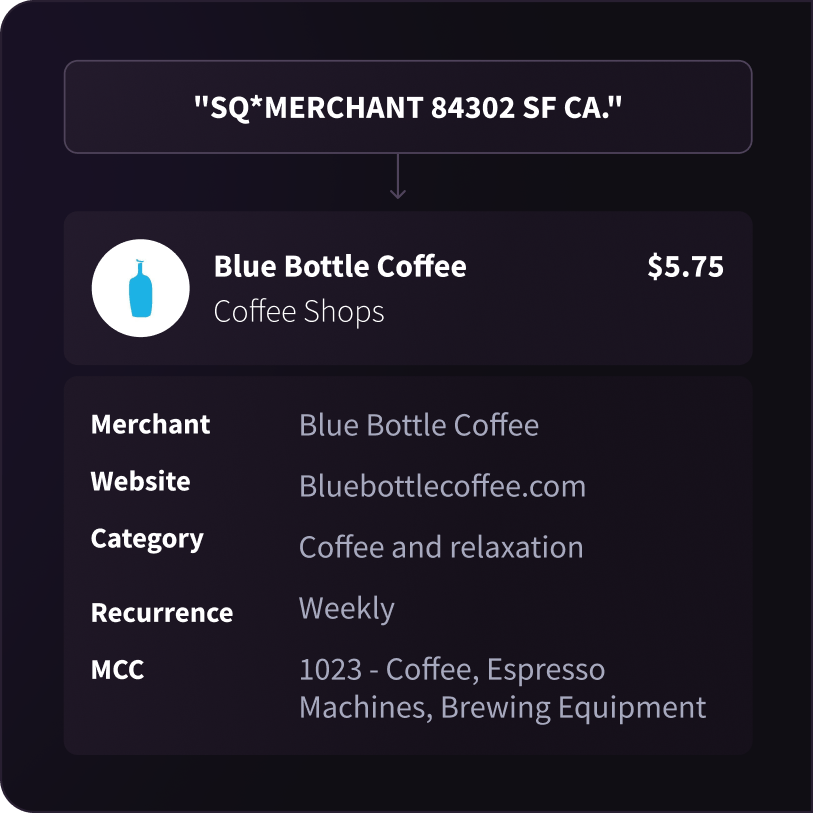

Coverage gets you the data. Enrichment makes it a decision.

Reaching the account is only half the job. The transaction feed that comes back is raw: cryptic merchant strings, no categories, no flag for which deposits are income and which are one-offs. Spreading that by hand is the old way. Seventeen macros for one loan.

What enrichment adds:

Categorized transactions

Rent, payroll, loan payments, transfers, and discretionary spend, labeled instead of guessed

Cash-flow attributes

Net cash flow, balance volatility, days negative, and NSF or overdraft counts

Identified income

Recurring deposits resolved into income streams, employers, and pay cadence

Risk signals

Loan stacking, returned payments, and patterns a single transaction never shows

Even aggregators that ship their own cash-flow products leave gaps. A specialized enrichment layer goes deeper, and Quiltt lets you reach it without a second integration. That is the difference between fetching transactions and fetching the signals you can actually underwrite on.

03

Income, asset, and identity verification, every provider's products through one API.

You shouldn't need a separate integration for every verification product. With Quiltt, bank-deposit income, asset balances, account ownership, and identity verification surface through the same normalized schema. Treat it as one income verification API for every provider's products, not a new integration per product.

For provider-specific products, like detailed income reports, asset verification statements, and instant account verification, Remote Data exposes the underlying aggregator response without a parallel integration. Your verification stack doesn't grow every time you add a provider.

Quiltt is the access layer, not a consumer reporting agency. The verification products themselves are delivered by the aggregator.

You get one integration and one normalized schema across every provider, whether Quiltt manages the credentials for you or you bring your own keys.

04

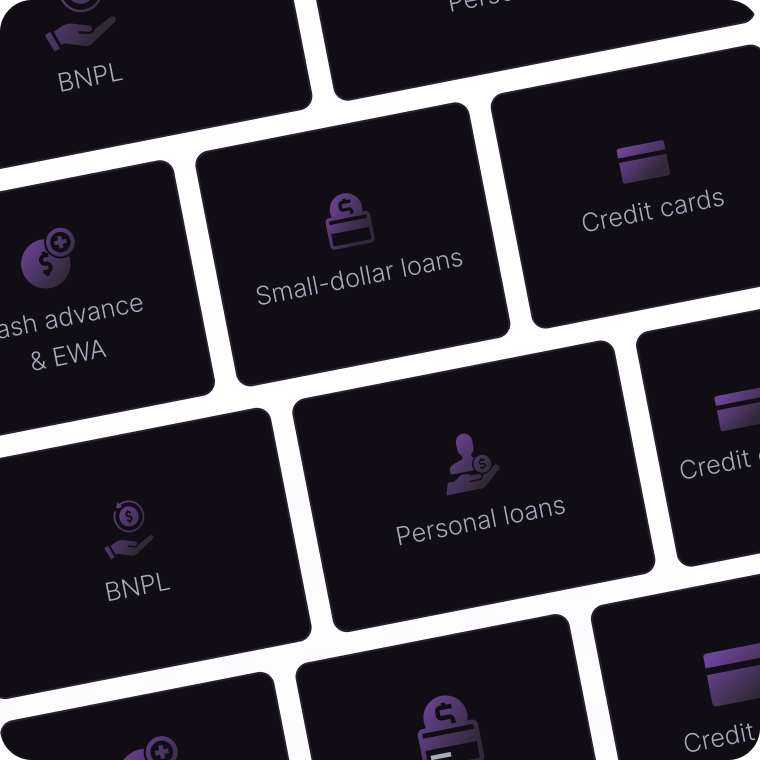

Built for every cash-flow lending model.

Different products lean on different signals, and the same Quiltt integration serves all of them. As we publish dedicated playbooks for each model, this page links out to the depth behind each one.

Cash advance & EWA

Timing is everything. Verify pay cadence and predict the next deposit so you can advance against real income, not a guess.

Small-dollar loans

Read balance volatility, overdraft history, and net cash flow to lend to thin-file borrowers without flying blind.

Credit cards

Look past the bureau file to income stability and existing obligations before you extend a line.

BNPL

Catch affordability risk and loan stacking across accounts before approval, at checkout speed.

Personal loans

Confirm income and model repayment capacity from real cash flow, not stated figures.

Frequently Asked Questions

Instant DemoVisit trust.quiltt.io to request the SOC 2 report and supporting security documentation. Quiltt shares these materials with builders and procurement teams under a standard review process.

Each token carries a defined scope that limits which accounts and data a connection can reach, so a compromised token exposes only that narrow slice. You can revoke a token at any time, which immediately cuts off access without affecting other connections.

No. Quiltt relies on OAuth 2.0 and tokenization, so end-user banking credentials never reach Quiltt's systems. Authentication happens at the financial institution, and Quiltt receives a scoped access token in place of a username or password.

Quiltt encrypts data in transit with TLS and data at rest with AES-256. Every connection between your application, Quiltt, and downstream providers travels over encrypted channels, so account and transaction data is never exposed in plaintext during transfer or storage.

Using a trusted financial account aggregator can help you stay compliant, especially if they support tokenized access, consent tracking, and audit trails. However, your app still needs to handle data responsibly, disclose usage in your privacy policy, and offer users the ability to revoke access.

Technically, yes, and AI tooling makes it easier than ever to do so. But this path is problematic:

- It puts customer credentials at risk

- It puts the company in potential conflict with bank terms of service

- It creates brittle infrastructure that breaks with any front-end change

- It undermines the open banking ecosystem that was specifically designed to prevent credential sharing.

For regulated fintech companies, the compliance and reliability costs of self-built scraping almost always outweigh the perceived short-term benefits.

Absolutely. At Quiltt, security is our top priority. We employ industry-leading encryption, secure authentication protocols, and adhere to the highest standards of data protection. Your data is always safe and secure with us.

Get started today

Your first sandbox pull takes five minutes.

No procurement, no gating, no surprise renegotiations. Sign up, connect, and see real data working in your product — today.