Quiltt for B2B Underwriting

You can’t underwrite a business you can’t see

Business cash-flow underwriting depends on seeing the operating account, and the operating account is rarely where consumer aggregators focus. A regional commercial bank, a business-banking fintech, a small credit union: any one of them can be the institution your single provider has never connected to. Quiltt routes across every major aggregator and picks whichever actually reaches that bank, so you don't miss the account that matters.

One API, every major aggregator, and the SMB underwriting data you need from wherever a business actually keeps its money.

01

The accounts consumer aggregators deprioritize.

A business doesn't bank like a consumer. The operating account sits at a regional commercial bank. Payroll and spend run through Brex or Ramp. Reserves sit at Mercury. Receivables land somewhere else entirely.

Consumer-focused aggregators optimize for the big retail banks where people keep their checking accounts. The commercial, regional, and fintech-native institutions where businesses actually operate get deprioritized, because there was always a shinier consumer use case to ship first. That gap is the exact place a business loan gets underwritten or declined.

Quiltt routes the connection across Finicity, MX, Akoya, and Plaid, picks whichever has the live connection to that institution, and returns a normalized record across every account.

What you get:

Coverage across regional commercial banks, business-banking fintechs like Brex, Ramp, and Mercury, and the long tail consumer aggregators skip.

Smart routing to the aggregator with the strongest live connection for each institution.

Automatic fallback when a connection breaks, so one bank never stalls an application.

"Your bank is not supported" is not an answer a business lender can afford. Quiltt makes sure the operating account is never the account you miss.

02

Verify the entity, then see cash across every account.

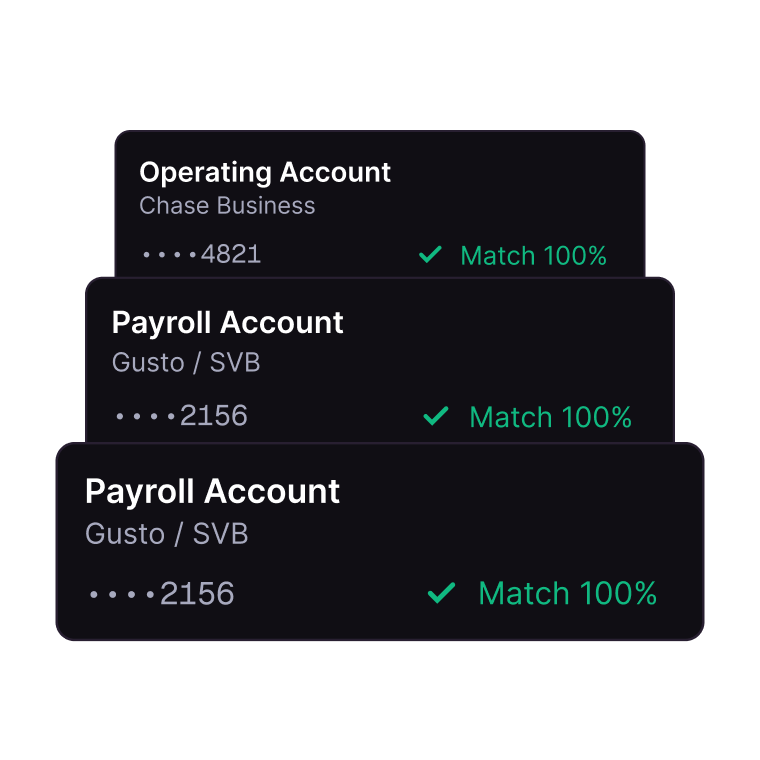

You're not verifying a paycheck. You're verifying that the business owns the accounts it claims, and that its real cash position supports the loan. With Quiltt, business account ownership verification and multi-account balance aggregation surface through one normalized schema. See total cash, runway, and the flow of revenue and obligations across every operating, reserve, payroll, and receivables account the business connects, not one account at a time.

What you can verify:

Business account ownership:

Confirm the legal entity owns the accounts on the application.

Cash position across accounts:

Total balances and runway aggregated across every connected account, not a single snapshot.

Revenue and obligations:

Recurring deposits, loan payments, and net burn, normalized across providers.

Provider-specific detail:

Via Remote Data when you need the underlying aggregator response.

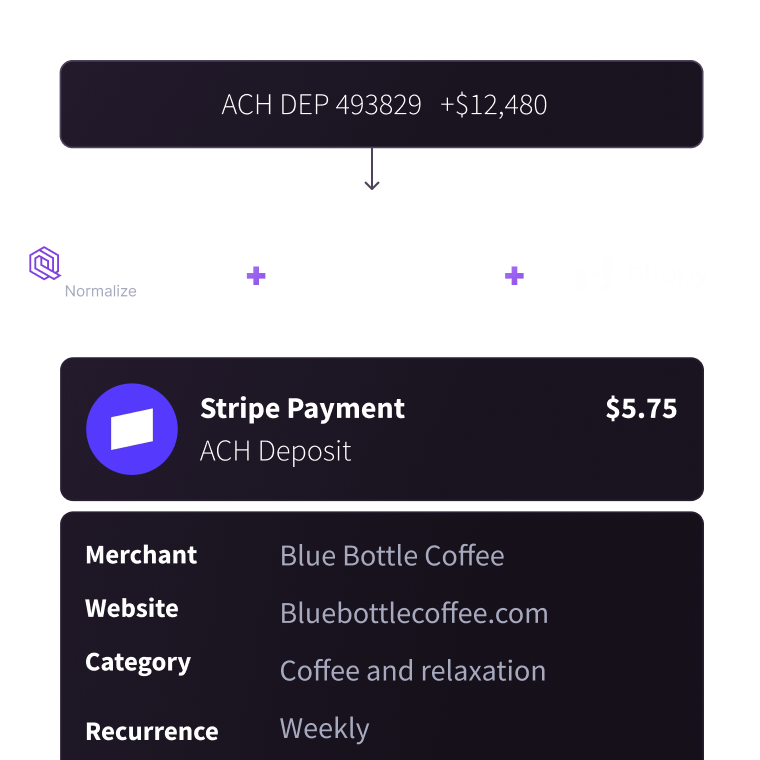

One more thing on data quality:

Connectivity moves the data, but context is what makes it usable. A revenue deposit misread as a loan draw can make a healthy business look volatile. Quiltt normalizes transactions across providers and, where you want it, enriches them through providers like Pave and Ntropy, so what reaches your model reflects how the business actually runs.

Quiltt is the access layer, not a consumer reporting agency. The verification products themselves are delivered by the aggregator. You get one integration and one normalized schema across every provider, whether Quiltt manages the credentials or you bring your own keys.

03

Business banking still runs on screen scraping.

That's your risk.

Most business bank data today still comes from screen scraping, and that is not fixing itself. The CFPB's 1033 rule is pushing consumer banking toward free, API-based, OAuth access. It does not cover business accounts. No mandate, no standard, no deadline. So while consumer connections move to permissioned APIs, business banking stays on the old rail.

Screen scraping logs into the bank as the borrower using stored credentials and parses the page. It breaks when the bank changes its UI, adds an MFA step, or flags the login as automation, and banks block it more aggressively every quarter.

For a lender that means connections that die mid-book, balances you actually pulled five logins ago, and bank passwords sitting in your environment as a breach you simply haven't had yet.

Quiltt takes the most durable connection available for each institution:

An OAuth API where one exists, where Finicity currently leads, and managed fallback where it doesn't. As more banks expose APIs, your pipeline moves onto them automatically, with no rebuild on your side. You get the best path that exists today, and a system that improves as the rails do.

04

A compliance and audit trail built for bigger loans.

Business loans are larger, and scrutiny scales with size. Quiltt is built so the data behind a credit decision can withstand an exam.

Every connection is permissioned by the business's authorized signer, OAuth-based wherever the institution supports it, FDX-aligned, and encrypted in transit and at rest. Webhook payloads are signed. Access is logged in detail.

When an examiner, auditor, or partner bank asks how a borrower's bank data reached your decision, you can show the whole chain:

Who authorized the access

Which institution and aggregator served the data, exactly when it was pulled

And when it was revoked

There are no stored bank passwords in your environment to defend. When a borrower relationship ends, revocation is clean and recorded.

For a regulated business lender, that audit trail isn't paperwork. It's the difference between a decision you can defend and one you can't explain.

05

Built for how business lenders actually underwrite.

Different products lean on different signals, and Quiltt serves them from one integration.

When an examiner, auditor, or partner bank asks how a borrower's bank data reached your decision, you can show the whole chain:

Merchant cash advance and revenue-based financing:

Size and time advances to real revenue deposits and daily cash flow, not last year's tax return.

Working capital and SMB term loans:

Read revenue trends, net burn, and runway across every account before you commit.

Equipment and construction financing:

Verify cash position and project inflows and outflows over a longer horizon, as draws and payments move across accounts.

Invoice factoring and AR financing:

See receivable inflows and customer payment patterns directly.

Business cards and charge cards:

Assess spend, obligations, and balance volatility for limits that adjust to the business.

Frequently Asked Questions

Instant DemoGet started today

Your first sandbox pull takes five minutes.

No procurement, no gating, no surprise renegotiations. Sign up, connect, and see real data working in your product — today.